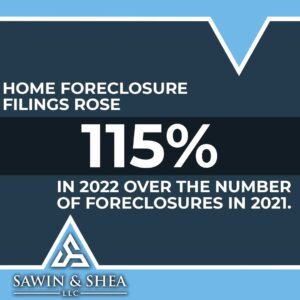

People file for bankruptcy for any number of reasons, from job loss to unpaid medical bills to an unaffordable mortgage. If you’re considering filing for bankruptcy, you’re not alone; roughly 375,000 people filed for bankruptcy in 2022, and home foreclosure filings rose 115% in 2022 over the number of foreclosures in 2021.

To many people, the most alarming thing about filing for bankruptcy is the possibility that they will lose their home. When facing dire financial circumstances, many people ask, “How can I pay off my overwhelming debt and also save my house from foreclosure?”

The good news is that homeowners can get back on their feet and keep their homes with various options to stop foreclosure. These include declaring Chapter 7 or Chapter 13 bankruptcy.

While both are good options to stop foreclosure (or postpone), in this blog we’ll focus on Chapter 13.

What to Do to Stop Foreclosure?

Unlike Chapter 7 bankruptcy, Chapter 13 does not require the filer to liquidate all their assets (including their home) to pay off creditors.

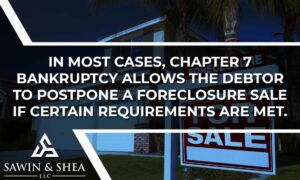

In most cases, Chapter 7 bankruptcy allows the debtor to postpone a foreclosure sale, but does not stop the process permanently.

Chapter 13 is a different animal. Sometimes referred to as a “wage earner’s plan,” Chapter 13 bankruptcy allows you to reinstate your mortgage as long as you have regular income and can commit to a payment plan in accordance with the court’s approval.

In other words, a Chapter 13 Plan can reorganize debts in ways that can help struggling homeowners get back on track with their mortgage payments, curing arrearages and making ongoing monthly payments. Unsecured debts like medical and credit card debt are forced to wait while you are given an opportunity to catch up. The unsecured debts receive a percentage (many times cents on the dollar) and are discharged at the end of a plan.

Your bankruptcy plan must comply with the bankruptcy code, which can be confusing for most, so it’s strongly recommended that a filer hire an experienced bankruptcy lawyer to guide them through the process and ensure everything complies with the bankruptcy code.

You cannot be a debtor under Chapter 13 or any other chapter unless you complete an approved credit counseling session (online or phone) within 180 days before filing. Your attorney can set you up with a company to accomplish this for you.

What Comes After a Chapter 13 Bankruptcy?

Once the bankruptcy process is complete and all mandated payments have been made, the filer is entitled to what is referred to as a discharge, meaning all debts are legally forgiven. Before the discharge process, the filer must be current on his or her mortgage payments and the court has issued an order to prove that it’s so.

However, before the bankruptcy is legally discharged, the filer must meet certain requirements, some of which are listed below: The debtor must:

- If applicable, certify that all debts owed to a spouse, former spouse, alimony, or other domestic support obligations have been paid

- Prove they have not received a discharge for another bankruptcy in the four years before declaring bankruptcy

- In some cases, complete a court-approved financial management course

Once received, the discharge releases the debtor from all debts in association with the payment plan (with limited exceptions). It also states that creditors may no longer start or continue an attempt to collect discharged obligations.

Should I See an Attorney?

Bankruptcy, as we’ve discussed here, is one of the best ways to keep your home if you’re buried in debt.

However, the laws around bankruptcy are complex and are constantly changing. For the best advice and guarantee that your bankruptcy process will proceed smoothly, your best choice is to hire an experienced lawyer.

And while It is legal to file for bankruptcy on a ‘pro se’ basis– i.e. without an attorney – in the vast number of cases this could have disastrous consequences. Bottom line: If you want your bankruptcy filing to succeed, hiring an attorney is the best way to ensure everything is accurate and in compliance with bankruptcy law.

An attorney with experience in bankruptcy law can help you with filings and guide you through the complicated, often confusing process. The Indiana bankruptcy attorneys at Sawin & Shea, LLC have been helping people navigate the bankruptcy process for years. If you’re wondering, “Can I save my house from foreclosure?” and considering filing for bankruptcy, call us at 317-759-1483 or request your free consultation online.