When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. Which decision you make or which one is the best decision can depend on your individual circumstances. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter 13 bankruptcy or a Chapter 7 bankruptcy.

If you are facing foreclosure or bankruptcy, the best way to determine which choice is right for you is to speak with an experienced bankruptcy attorney. In this article, we will offer you guidance, but speaking with an attorney one-on-one can provide you with a better understanding and a more personalized solution.

If you have questions and are considering bankruptcy, don’t hesitate to reach out to our team at Sawin & Shea, LLC for assistance.

What’s the Difference?

A foreclosure is a process used by mortgage lenders to recover their money when a homeowner defaults on their mortgage payments. During this process, the lender will typically repossess the house and then sell it off at a public auction. A bankruptcy, on the other hand, is a process that debtors can use to eliminate some of their debt or establish a payment plan for their debts so they can potentially save some of their assets or property.

Bankruptcy vs. Foreclosure: Which is Worse?

Before you can decide which option is worse or which is best, it helps to understand the difference involved in these two processes, which are laid out in the table below:

| Bankruptcy | Foreclosure | |

| Who initiates? | The individual (you) | The lender |

| Who controls the property? | After initiating bankruptcy, you may be able to retain control of the property until the case is finalized through an “automatic stay” order | The lender |

| After the case | You could potentially keep your home. If there are any leftover debts, they will be discharged when the case is closed | The house will be sold and you may still owe money to the creditor if the proceeds don’t cover the debt |

| Future home purchase restrictions | None | Eligible to buy again in five years with restrictions or in seven years without restrictions |

| Loan reporting | Will be reported on future loan applications | Will be reported on future loan applications |

Pros and Cons to Both

Which is worse, bankruptcy or foreclosure? This depends on your attachment to the home. In a foreclosure, you will without a doubt lose the home and you could end up owing money if the sale does not cover your debt. With bankruptcy, however, you could potentially keep your home.

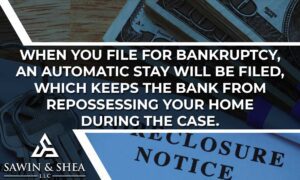

When you file for bankruptcy, an automatic stay goes into effect, which keeps the bank from repossessing your home during the case. As part of the bankruptcy process, you could end up keeping your home. However, bankruptcy does not always stop a foreclosure from happening. You could still end up having to surrender the home to your lender. However, the difference is that after this happens and the bankruptcy is finalized, if there are any remaining debts, they will likely be discharged.

Bankruptcy Chapter 13 vs. Foreclosure

There are two types of bankruptcies that you could file for if you are facing foreclosure. In a Chapter 7 bankruptcy, you might not be able to ultimately keep your house from being surrendered to the lender. However, at the end of Chapter 7, any remaining debts will be discharged, so you will not end up owing a deficiency claim on the foreclosure.

In Chapter 13, you may be able to keep your home, but you will have to work out a payment plan, so you will still have to pay money to your lender. Most Chapter 13 payment plans last three to five years.

In a foreclosure, you will lose the house, and whether you owe money or not will depend on whether or not the sale covers the debts. In Chapter 13, you will keep the house, but you will have to make enough money to make payments for three to five years.

Bankruptcy vs. Foreclosure On Credit Report

Both options aren’t ideal with regard to your credit score. A foreclosure will remain on your credit report for seven years, whereas a bankruptcy will remain for seven or ten years. However, while bankruptcy may affect your credit score for longer, it is considered the better option. This is because foreclosures are viewed more seriously by lenders than bankruptcies that don’t include the house.

How Sawin & Shea, LLC Can Help

At Sawin & Shea, we provide compassionate and understanding representation to those struggling with debt and filing for bankruptcy. If you are facing foreclosure and want to consider bankruptcy as an alternative, we are here to help.

Contact us at 317-759-1483 or send us an email for a free consultation today!